Top organizations use open source they include Google, Facebook, Microsoft, Amazon, IBM, Twitter, Red Hat, Uber, Airbnb, and Netflix.

Why are banks and hedge funds suddenly into open source. Past practices have indicated that banks are very competitive and cautious of their proprietary data.

Since they handle confidential data, they’ve been expected to keep secrets. For example, in 2009 Goldman Sachs had an employee jailed for allegedly stealing their proprietary software.

However, 8 years later in 2017 Goldman Sachs launched three of its latest open-source projects – Jrpip, Obevo and Tablasco – on GitHub. They also have an in-house language, Legend, that is now open source.

In the creation and use of open-source tech-based companies outperform financial businesses. For instance, Google has 70 open-source projects. The largest of them all is Android which is 75% of what all smart phones use.

Why Organizations Choose Open-Source

As a result, banks in 2023 will increasingly adopt open-source technology, as they are under pressure to innovate and remain competitive. This shift is driven by a desire to gain access to new and emerging technologies, such as machine learning and blockchain, to improve customer experience and reduce operating costs.

Banks are opting for open-source technology because

- Cost Savings: Open source saves costs by eliminating the need to pay for expensive proprietary software licenses and reducing development costs by leveraging existing open-source solutions.

- Customization: It can be customized to fit an organization’s unique needs, as opposed to proprietary software which may be more rigid.

- Security: Is more secure because vulnerabilities can be quickly identified and addressed by the community of developers.

- Innovation: Foster innovation by allowing organizations to collaborate and share ideas with others in the community.

- Reliability: Open source has proven to be reliable and stable in mission-critical applications. For example, the Linux operating system is widely used in mission-critical applications such as space missions and stock exchanges.

- Community Support: Open-source communities can guide and assist organizations with their projects, including bug fixes and development advice. The Apache web server project is an example of a project that benefits from a large and active developer community for ongoing support

- Future Outlook: More organizations are likely to adopt open-source solutions, like Red Hat Enterprise Linux, which provides a secure and stable operating system that can be tailored to meet specific business needs.

In addition, open-source software is flexible to customize to specific needs. This allows banks to develop innovative applications that leverage the latest technologies, such as AI and machine learning, to understand customer behavior and anticipate their financial needs.

Real-Life examples of Open-Source Technology Adoption

One example of open-source technology being adopted by banks is the operating system Linux. Banks such as ING, UBS and JPMorgan Chase have implemented Linux powered systems to better manage their IT infrastructure. They use it to:

- Host their IT infrastructure and provide a secure computing environment.

- Develop custom applications, such as mobile banking and digital wallets.

Other open-source projects that are popular in the banking sector include:

- Apache Kafka, an event streaming platform

- Hadoop, a big data analytics platform

Historically banks have been hesitant to adopt open-source software; where software source code is shared and made freely available). With traditional vendors like IBM, TIBCO, Oracle strongly positioned in this industry, the move to open source has been slow.

In recent years, forced by a rapidly changing business, banks are transforming their IT organizations considerably, adopting new technologies and methodologies like Cloud, microservices, Open APIs, DevOps, Agile and Open Source. Because often the above adoptions enforce each other.

The Open-Source movement has reached maturity. While 5-10 years ago, it was associated with computer-nerds, idealists and small start-ups, today it is mainstream. The recent acquisitions of open-source companies by large established corporate tech-vendors is the best proof of this evolution:

- SalesForce bought MuleSoft for $6.5 billion in March 2018

- Microsoft bought GitHub for $7.5 billion in October 2018.

- IBM purchased Red Hat for $34 billion in 2019

At the same time these incumbent tech players are adopting open-source strategies themselves. For example, Microsoft, initially one of the most guarded, has adopted an open-source strategy, since Satya Nadella became CEO in 2014. Examples of its open-source technologies include:

- Edge: The Edge browser is switching to the Google based open-source chromium platform

- .NET framework: the full .NET framework was open-sourced on Git-Hub

- Windows 10: built on open-source Progressive Web App technology

- Windows 11: analysts speculate that the NT kernel would be (gradually) replaced by the Linux kernel

- Azure platform: the most used operating system on Microsoft Azure is not Windows Server, but rather Linux

- Open-source contribution: Microsoft has become the largest contributor to open source in the world. It is more active than the second most active contributor, Google. There are 20,000 Microsoft employees on GitHub and over 2,000 open-source projects

The Different Stages of Open-Source Adoption

Open-source software has many benefits for banks, but it requires a cultural shift in the whole organization, which takes time and intensive change management.

Banks can start adopting open-source software in different ways. They can start by using open-source software where possible, either as full solutions or as components they combine to build custom applications.

As they become more familiar with open-source software, banks can start contributing back to the community by identifying bugs and implementing valuable features. By doing so, banks improve their corporate image and benefit from future testing and extensions by the community.

The final step is to open the bank’s existing proprietary software, which is the most complex and time intensive.

First, banks fear their code will be scrutinized in public, resulting in a brand risk and potentially exposing security issues. Additionally, some bank leaders may fear giving away competitive advantage.

Second, depending on the kind of open-source software. How complex is it? Banks should first gain experience with low-level abstraction open-source software, like:

- Databases (MySQL, Mongo DB, Cassandra and Postgres),

- Middleware (WSO2, Kafka, Apache Camel, Envoy, Istio)

- Operating systems (Linux and Kubernetes)

Gradually they can move up the stack to higher level of abstractions, like:

- Business process (jBPM)

- Task management tools

Finally, they can use also open source for the financial core processes. These include, Cyclos, Mifos X / Apache Fineract, MyBanco, Jainam Software, OpenCBS, OpenBankProject, Cobis, OpenBankIT, Mojaloop).

Contributing to Open-Source

Ultimately the banks’ software should have at its core open-source software, except for solutions exclusively offered via SaaS.

Many banks already use open-source software and prefer it over proprietary software. More banks are contributing to open-source projects or open-sourcing their own software. Some examples of such banks include:

- Capital One’s, one of the largest credit card companies in the US, has been on a digital transformation journey over the past 6 years.

- Goldman Sachs recently open sourced its proprietary data modeling program Alloy

- J.P. Morgan Chase released code on GitHub for multiple initiatives; its Quorum blockchain project.

- Deutsche Bank open-sourced multiple projects, like Plexus Interop (from its electronic trading platform Autobahn) or Waltz (IT estate management

The Dilemma of Open-Sourcing In-House Software

The move of some banks to open-source proprietary software seems strange at first sight, as intelligent software has become the competitive edge of any bank. Nonetheless banks have a lot to gain in using (adopting) open source and contributing to it:

5 Benefits of using open-source software:

- Lower costs: avoid the exuberant annual software license costs paid to software vendors.

- Reduce time-to-market: allowing developers to bolt together pre-existing modules rather than having to create them all from scratch, allows to considerably reduce development time.

- Easily customizable: open-source software can be customized, allowing to provide the golden means between buying a software package from a vendor (quick time-to-market, but limited customization possibilities) and internally custom-built software.

- No vendor lock-in

- Lower learning curve for new joiner

7 Benefits of Contributing to Open-Source Software:

- Good for corporate image through giving back to the community.

- Transparency: open-source software is intrinsically more secure than proprietary software, where the code is kept a secret.

- Easier hiring of resources, as IT resources like to work on open-source and good potential candidates can be identified by looking at public commits of externals to the bank’s open-source projects

- Motivation: often IT resources at banks feel a lack of social commitment. Contributing back to open sources can give them a feeling of pride and giving back to community.

- Cultural accelerator: open-source communities promote collaboration, almost always remote and often across different time zones and cultures. Collaborating in such an environment will make the bank IT department better and more adapted for future evolutions.

- Gain from testing and extensions built by contributors outside the bank

- Facilitates collaboration between different banks on shared concerns like KYC (Know Your Customer) and AML (Anti-Money Laundering)

5 Fears of Making In-House Software Open-Source

Even though open source has many advantages, there are still some banks that are hesitant to use it. These banks are especially hesitant to contribute to open source or share their own software. Here are some reasons:

- Contractual and legal: Various types of open-source software license models exist which can make it challenging for large banks to comply with all the terms and conditions. But tools like FOSSA, DejaCode, WhiteSource, Code Janitor help monitor and follow-up the compliance on open-source licenses.

- Support: Banks worry about a lack of support when using open-source tools. However, many open-source tools offer corporate support. If not, the bank IT teams should engage with the open-source community to resolve an issue.

- Compliance and security: There are risks when publishing source code on the internet that criminals can find loopholes in the code. While open-sourcing code ultimately leads to more secure software.

- Losing Competitive advantage: Most internal banking software is commodity software that doesn’t provide any differentiation. Open sourcing these applications can free up resources to work on real value-added services.

- Brand risk: Banks are concerned that open-sourcing bad software can harm corporate branding

How Does Open-Source affect FinTech

If banks start using a lot of open-source software, will FinTech’s new software services offer to banks, fail?

Fortunately, fintech has already moved from an annual license model to newer partnership models. Using cloud technology and Open APIs has made it hard to justify annual licenses.

Partnership models are now used instead of software license costs. These include:

- PaaS (Platform as a Service), SaaS (Software as a Service) and Baas (Business as a Service) models

- “Open core” models (also called Dual licensing). Here, the core of the software is delivered for free and open source. However, the tooling for large corporations are license based

- Support model: pay a party for access to a support desk and providing updates on when new versions should be installed

- Service model for profits; training services, implementation services, customizations to the open-source software at request of the banks.

Making an open system of collaboration between FinTech and banks will lead to better services for everyone. Banks should understand that technology is important for their business.

They should learn from the big technology companies by hiring the best people, using existing software, and supporting quick changes with DevOps and Agile methods. Banks can use open-source strategies to achieve this goal.

References:

]]>

The future of finance is changing rapidly. Over the past decade, advanced machine learning has taken over many tasks that humans previously performed.

From self-driving cars to smart phones, these technologies have advanced at an exponential rate. Now, new technologies are emerging that use artificial intelligence (AI) to complement existing processes and provide insights that allow people to make better decisions.

In November 30th 2022 Open AI launched ChatGPT. By December 4th the open platform had over a million users, breaking the records other popular platforms.

Facebook took up to 10 months before accumulation one million users. Twitter took up to 2 years to get to a million users. Last but not least, TikTok, The Open AI innovation received up to 1million users in 24 hours.

The amount of posts on LinkedIn and YouTube about the supposed solution to all repetitive tasks were uncontrollable. Experts have mixed reactions to the possibilities of AI, some agree that it’s impact has been far-reaching and positive so far.

Understanding the impact of AI on finance services

Today, AI is an integral part of our lives. From self-driving cars and video games to Netflix’s recommendation engine and Facebook’s algorithm, AI is no longer just in our pocket (it’s in everything).

But what has this changed for the financial services industry? What are the biggest risks and opportunities that it can bring? And how will AI impact your role in finance moving forward?

According to the mckinsey-tech-trends-outlook-2022-research-overview.pdf Applied AI received $165 billion investment funding in 2022.

Through the machine learning Canonical stack, we are witnessing the democratization of AI. The use of artificial intelligence will aid in the management of credit card fraud risks and the prevention of losses.

The benefits of AI in the financial industry

The benefits of AI in the financial industry are manifold. The technology is expected to reduce the costs of customer service and improve efficiencies across all stages of the process. It will also enable banks to enhance their product offerings and offer tailor-made services to customers.

The introduction of AI technologies is expected to provide financial institutions with a competitive advantage, enabling them to better adapt to the rapidly changing market environment.

AI has been a major buzzword for years now and has become a popular topic of discussion as we aim to reinvent our future. As AI becomes mainstream here are some benefits the financial industry will enjoy:

● Lower costs by automating repetitive tasks that take up a lot of time.

● Improved customer experience through personalized recommendations and personalization.

● Improved efficiency by utilizing machine learning algorithms to make better decisions.

● Increase in revenue through improved market research and analysis.

The financial services industry is undergoing a transition as AI becomes more pervasive. It’s no longer about the mythical replacing humans with machines, but leveraging artificial intelligence to better serve customers and improve operations.

In fact, AI can play a key role in helping banks and other financial institutions create value for their customers and deliver a better customer experience.

Here are some ways AI will improve the customer’s journey:

1. Improving customer service: Analyzing data from transactions and account activity to identify trends that can be used for predictive analytics. For example, AI could analyze historical transaction data and identify trends such as when customers purchase certain products or make payments on time. This allows banks to predict which customers might need assistance in the future.

2. Automating tasks: AI can automate many of the tasks currently done manually, freeing up employees for customer support. For example, an AI system might be able to integrate information from multiple sources, such as account statements, credit scores and social media posts, into a single report that shows the entire picture of your finances in real time.

3. Predicting client behavior: With enough data about customers’ past spending habits, an AI system could predict what they’re likely to want in the future.

4. Decision support systems, which are based on data analysis and machine learning algorithms, can assist in making financial decisions (DSS).

The impact of AI on finance is that it can automate many manual tasks, freeing up time and resources for humans to focus on higher-value activities. These include:

1. Predicting future events, such as the weather or stock prices, which could be used to make better investment decisions.

2. Creating original content, such as articles and videos, which can be shared with customers in order to drive engagement and loyalty.

3. Insights into customers’ behavior and preferences, which will help them understand how best to serve them. AI can analyze large amounts of financial data to forecast future outcomes or trends, a process known as advanced analytics or big data analytics (aka BDaaS).

Predictions for the adoption of AI in 2023

Artificial intelligence (AI) leaders, consultants and vendors looked at enterprise trends and made their predictions. After a whirlwind 2022, here are some quoted highlights of their insights:

1. AI will be at the core of connected ecosystems —–Vinod Bidarkoppa, CTO of Sam’s Club and SVP of Walmart

In 2023, we’re going to see more organizations start to move away from deploying siloed AI and ML applications that replicate human actions for highly specific purposes and begin building more connected ecosystems with AI at their core.

This will enable organizations to take data from throughout the enterprise to strengthen machine learning models across applications. Hence effectively creating learning systems that continually improve outcomes.

For enterprises to be successful, they need to think about AI as a business multiplier, rather than simply an optimizer.

2. AI will create meaningful coaching experiences— Zayd Enam, CEO, Cresta

Modern AI technology is already being used to help managers, coaches and executives with real-time feedback to better interpret inflection, emotion and more, and provide recommendations on how to improve future interactions.

The ability to interpret meaningful resonance as it happens is a level of coaching no human being can provide.

3. AI will empower more efficient DevOps – Kevin Thompson, CEO, Tricentis

When it comes to devops, experts are confident that AI is not going to replace jobs; rather, it will empower developers and testers to work more efficiently. AI integration is augmenting people and empowering exploratory testers to find more bugs and issues upfront, streamlining the process from development to deployment.

In 2023, we’ll see already-lean teams working more efficiently and with less risk as AI continues to be implemented throughout the development cycle.

“Specifically, AI-augmentation will help inform decision-making processes for devops teams by finding patterns and pointing out outliers, allowing applications to continuously ‘self-heal’ and freeing up time for teams to focus their brain power on the tasks that developers actually want to do and that are more strategically important to the organization.”

4. AI investments will move to fully-productized applications — Amr Awadallah, CEO, Vectara

There will be less investment within Fortune 500 organizations allocated to internal ML and data science teams to build solutions from the ground up. It will be replaced with investments in fully productized applications or platform interfaces to deliver the desired data analytic and customer experience outcomes in focus.

That’s because in the next five years, nearly every application will be powered by LLM-based neural network-powered data pipelines to help classify, enrich, interpret and serve.

But productization of neural network technology is one of the hardest tasks in the computer science field right now. It is an incredibly fast-moving space that without dedicated focus and exposure to many different types of data and use cases, it will be hard for internal-solution ML teams to excel at leveraging these technologies.

References

ai-trends-for-2023-industry-experts-and-chatgpt-ai-make-their-predictions/

AI is Changing Financial Services Delivery

AI is transforming the way businesses operate and invest, enabling them to identify patterns, make predictions, create rules, automate processes, and communicate more efficiently.

It is at the top of the agenda for financial services, as customers are becoming more informed and expect transparent as well as consistent and reliable services.

To generate value, banks and financial services organizations should be smart about choosing appropriate use cases and technologies. These use cases should outline what “measurable” success looks like both in the short and long term and should be assessed and prioritized based on the level of business impact and technological feasibility.

For example, classification type problems are commonly seen in banking, and AI-driven call center compliance automation is an example of using AI to classify high-risk calls for further review.

Mariette van Niekerk leads the Data Science & AI practice of Deloitte New Zealand’s Risk Advisory team, using a variety of machine learning / AI technologies to detect and manage fraud and operational risks.

She is a seasoned data scientist and project manager with a 12-year track record of delivering cross-industry operations research and artificial intelligence solutions. She recommends breaking the high-level plan for full roll-out down into smaller phases that deliver benefits early.

References

“How AI Is Shaping the Future of Financial Services.” Deloitte New Zealand, 18 May 2022

Challenges of Adopting AI in the Financial Industry

The use of AI in global banking is estimated to grow from a $41.1 billion business in 2018 to $300 billion by 2030. Traditional financial services companies have two objectives to fulfill with AI: speed, flexibility, and agility, and adhering to compliance standards and regulatory requirements.

However, big challenges remain in building responsible and ethical AI systems, and traditional financial institutions struggle to deploy in-depth AI capabilities to truly harness its full potential.

These include:

Data quality and weak core structures make it difficult for AI and ML systems to identify overlapping and conflicting entries.

Lack of support for AI-specific scale and volume and can even show biased results when written by developers with a biased mind.

Lack of standard processes and guidelines for AI in the financial domain.

The lack of talent, budget constraints.

Significant commitment toward AI investment. It is important to consider the context, use case, and type of AI model implemented to analyse the appropriate approach while collaborating or upscaling core tech systems.

The Economist’s research team found that 86% of Financial Service executives plan to increase AI-related investment over the next five years, with the strongest intent expressed by firms in the APAC and North American regions.

Businesses that scale with AI over time, will enjoy an unwavering focus on compliance, customer satisfaction, and retention.

References

AI Adoption Challenges in Traditional Financial Services Companies, 7 Mar. 2022

Role of Government and Regulatory Bodies in Financial Services AI

AI, including machine learning (ML), can improve the delivery of financial services as well as operational and risk management processes. Financial authorities are encouraging financial sector innovation and the use of new technologies.

As a result, sound regulatory frameworks are required to maximize benefits and minimize risks from these new technologies. There are AI governance frameworks or principles that apply across industries, and several financial authorities have begun developing similar frameworks for the financial sector.

These frameworks are based on general guiding principles such as dependability, accountability, transparency, fairness, and ethics. Financial regulators are under increasing pressure to provide more concrete, practical guidance.

Existing governance, risk management, and development and operation requirements for traditional models also apply.

{kind=link}

Businesses can benefit from this financial industry behemoth of JP Morgan. This section examines how one of the largest banks, JP Morgan Chase & Co. is using artificial intelligence to tackle a slew of mundane tasks.

The multinational is unwavering in its commitment to lowering costs, increasing operational efficiency, and

improving the client experience, and it has been an early adopter of disruptive technologies such as Blockchain.

They established a center of excellence within Intelligent Solutions in 2016 to investigate and implement a

growing number of use cases for machine learning applications across the organization.

They have a document review system, in which corporate lawyers analyse large amounts of data and sort and identify important pieces for litigation, which is one of the legal profession’s pain points.

According to a McKinsey & Co. study, nearly a quarter of lawyer work output can be automated. According to a study conducted by Frank Levy at MIT and Dana Remus at the University of North Carolina School of Law,

implementing machine learning could reduce lawyers’ billable hours by about 13%.

JP Morgan has also implemented a program called COiN, which uses unsupervised machine learning to automate the contract document review process. The primary technique employed is image recognition, and the algorithm can extract 150 relevant attributes from annual commercial credit agreements in seconds, as opposed to 360,000 person-hours for manual review.

COiN is proving to be more cost-effective, efficient, and error free, and the company is committed to its technology hubs for teams specializing in big data, robotics, and cloud infrastructure in order to find new revenue streams while reducing expenses and risks.

References:

“AI in Banking: A JP Morgan Case Study and Takeaway for Businesses.”

Conclusion

In conclusion, the current state of Artificial Intelligence in banking is rapidly evolving and has the potential to greatly improve the efficiency and accuracy of financial services. AI-powered solutions can help banks with tasks ranging from fraud detection to customer service and personalization.

However, the implementation of AI in the banking sector must be done with caution and proper regulations in place to ensure the safety and privacy of customers’ data and to prevent any potential biases in decision making.

As AI continues to mature, it is expected to bring significant benefits to the banking industry and its customers, and it is essential for banking executives to stay informed and proactive in incorporating AI technology into

Source: Atul Kumal from Linkedin

APIs can bring value to a company by helping with innovation and development, but only a few can make money directly. A good API strategy can help simplify things and save money in the long run. To build a successful API strategy, consider these steps:

- Decide on the strategy based on the business, target audience, and API usage.

- Organize APIs based on data sensitivity, importance, and usage.

- Make sure the APIs you choose are valuable.

- Set up different portals, security measures, and paths for internal and external users.

- Measure the success of your APIs using metrics.

- Have a service level agreement policy that considers your backend capacity.

Having a clear API strategy can help simplify things and save money in the long term. It also has these benefits:

- Helps you understand things faster

- Gives you confidence in your investments

- Makes things more flexible

- Prevents things from getting too complicated

- Let’s communicate changes easily across the company.

Source is API Expert David Roldan

An Introduction to Monetizing APIs in the Banking Industry

The African banking industry has been rapidly evolving in recent years, with a growing emphasis on digital transformation and innovative financial technology solutions.

One area that is gaining traction in the region is the monetization of APIs (Application Programming Interfaces) in the banking sector.

APIs are the building blocks that enable financial institutions to expose their systems and data to third-party developers, who can then create new financial products and services based on this data.

By monetizing their APIs, banks can generate new revenue streams, enhance their brand, and improve customer engagement.

An example of this in Africa is the Kenya Commercial Bank (KCB), which has been a leader in the use of open APIs in the region. The bank has made its APIs available to developers, allowing them to create innovative financial products and services based on KCB’s data and systems.

This has helped the bank to increase its revenue and improve its customer engagement, as well as enhancing its reputation as a forward-thinking financial institution.

Another African bank that has embraced the monetization of APIs is Standard Bank Group, based in South Africa. The bank has created a platform called Open API that enables developers to build new financial products and services using Standard Bank’s systems and data.

This has helped the bank to generate new revenue streams and improve its customer engagement, while also establishing it as a leader in the field of API monetization.

In conclusion, the monetization of APIs in the African banking industry is a growing trend that has the potential to bring significant benefits to financial institutions in the region.

By making their systems and data available to developers, banks create new revenue streams, enhance their brand, and improve customer engagement, while also contributing to the development of the African financial technology ecosystem.

The Benefits of Open Banking for Banks and Financial Institutions

Open banking is a financial system where banks and other financial institutions make customer data accessible to authorized third-party providers. This allows customers to manage their financial information and payments through a variety of apps and services (multi-channel).

In the African banking industry, open banking gained significant traction in recent years. It is poised to revolutionize the way banks and financial institutions operate.

In this section, let’s explore the key benefits of open banking for banks and financial institutions in Africa.

- Improved Customer Experience: Open banking enables banks to offer customers a more seamless and convenient banking experience. For example, customers can access their financial information and make payments from a single app, without having to log into multiple bank accounts. This results in a better user experience and increased customer satisfaction.

- Increased Efficiency: Open banking allows banks to automate many manual processes, such as account opening and loan application. This results in increased efficiency and reduces operational costs.

- Enhanced Security: Open banking mandates strict security measures, such as two-factor authentication and encryption, to protect customer data. This enhances security and reduces the risk of fraud.

- New Revenue Streams: Open banking enables banks to partner with fintech companies and offer new and innovative financial services. This creates new revenue streams and helps banks stay competitive in a rapidly evolving market.

- Improved Data Analytics: Open banking allows banks to access a wealth of customer data, which can be used to gain insights into customer behavior and preferences. This information can be used to improve product offerings and target customers more effectively.

Examples from the African banking industry show the potential benefits of open banking. For example, Standard Bank in South Africa has partnered with fintech company TymeBank to offer customers a new way to bank.

The partnership has enabled Standard Bank to reach a new customer base and offer innovative financial services. Another example is Absa Bank in Kenya, which has implemented open banking to streamline its operations and offer customers a more convenient banking experience.

References:

TymeBank ropes in TFG to expand its footprint

Strategies for Monetizing APIs in the Financial Services Industry

Application Programming Interfaces (APIs) have become a crucial aspect of the financial services industry. They enable banks and other financial institutions to offer customers seamless and innovative services.

In the African banking industry, APIs have the potential to unlock significant revenue streams, but realizing this potential requires careful planning and execution.

In this section, we’ll explore some of the strategies for monetizing APIs in the African financial services industry.

- Charge for Access: One of the simplest ways to monetize APIs is to charge for access. Banks can charge third-party developers and fintech companies for access to their APIs. This enables them to offer new and innovative financial services to customers.

- Offer Premium Features: Banks can offer premium features through their APIs, such as enhanced security and increased transaction limits. These premium features can be offered at an additional cost. This provides a new revenue stream for banks.

- Leverage Data: APIs provide banks with access to valuable customer data, which can be used to gain insights into customer behavior and preferences. This data can be monetized by selling it to third-party companies or using it to develop targeted marketing campaigns.

- Partner with Fintechs: Banks can partner with fintech companies to offer new and innovative financial services through their APIs. This creates new revenue streams and helps banks stay competitive in a rapidly evolving market.

Statistics show the growing importance of APIs in the African financial services industry.

For example, a recent study found that the number of fintech companies in Africa has increased by 50% in the past five years, driven in part by the increasing use of APIs.

Another study found that the value of the African fintech market is expected to reach $2.2 billion by 2023, driven by the growth of APIs.

Examples from the African banking industry demonstrate the potential of monetizing APIs.

For example, Standard Bank in South Africa has developed a comprehensive API platform that enables third-party developers to build financial services on top of its platform.

This has allowed the bank to generate new revenue streams and offer innovative services to customers.

Another example is Absa Bank in Kenya, which has implemented a robust API platform that enables it to partner with fintech companies and offer new financial services.

The Future of Banking with Open Banking and APIs

The African banking industry has undergone significant changes in recent years, driven by technological advancements, increased competition, and changing customer needs.

The introduction of open banking and APIs has further transformed the industry, providing new opportunities for growth and innovation.

APIs, or application programming interfaces, are a key component of open banking, providing secure and efficient connections between different systems and platforms.

In Africa, the adoption of open banking and APIs has been slow compared to other regions, but it is gradually gaining momentum.

A recent survey of African banks found that only 17% currently offer open banking services, but nearly 60% plan to do so within the next two years. This indicates a strong demand for these services and a recognition of their importance for the future of the banking industry.

Some of the benefits include:

- Increased competition and innovation. By allowing third-party providers to access financial data, banks can better understand their customers’ needs. They also align preferences and offer more personalized and relevant products and services. This, in turn, leads to increased customer satisfaction and loyalty.

- Increased efficiency and cost savings. By using APIs, banks can automate many processes, such as account opening and customer onboarding. This reduces the time and resources required to perform these tasks. This leads to lower costs and improved profitability for banks, as well as faster and more convenient services for customers.

Real-World Examples of Banks Monetizing APIs and Open Banking

The implementation of open banking and APIs has provided a new avenue for banks to monetize their services.

Real-world examples of banks monetizing APIs and open banking in Africa exist, showcasing the potential of this new technology.

- Charge third-party providers for access to their data and services. For example, a bank may offer API access to its payment’s infrastructure. This allows third-party providers to build new financial products and services that integrate with the bank’s platform. In exchange, the bank may charge a fee for each API call made by the third-party provider.

- Offer premium services to customers. For example, a bank may offer customers access to their financial data through an API. Hence customers easily manage their finances and make better-informed decisions. The bank can charge a fee for these premium services, providing a new revenue stream.

Regulators have an important role to play in supporting the monetization of APIs and open banking in the African banking industry.

Regulators are responsible for establishing standards for data protection and security, ensuring that customer data is handled in a safe and secure manner.

Regulators can also encourage innovation by supporting the development of new financial products and services that make use of open banking and APIs.

Regulators also have a critical role to play in ensuring the success of this new technology, by establishing clear standards and practices.

Preparing for the Future of Banking with a Strong API Strategy

To remain competitive in an increasingly crowded marketplace, banks in Africa must prepare for the future of banking by developing a strong API strategy.

This includes investing in technology, training employees, and establishing partnerships with third-party providers to drive innovation and growth.

By embracing APIs and open banking, banks can position themselves for success in the years to come.

Source: Pixabay

Understanding the Role of APIs in Digital Transformation of Banking:

APIs have emerged as a critical component of digital transformation in the banking industry:

- Helping banks connect and integrate different systems and platforms.

- Improve customer experiences.

- Increase efficiency and drive innovation.

In the African banking industry, the adoption of APIs has gained momentum in recent years, with major banks such as Standard Bank, First National Bank, and Absa Group, among others, leading the way.

For example, Standard Bank has used APIs to launch its “Open Up” platform, which enables businesses to access its financial services programmatically.

Best Practices for Securing APIs in the Banking Industry:

With the increasing use of APIs in the banking industry, it is imperative to ensure their security to protect sensitive customer information and maintain public trust.

Best practices for securing APIs in the banking industry include implementing robust:

- Authentication and authorization processes

- Using encryption to secure sensitive data

- Regularly monitoring and testing API security

For example, Absa Group has put in place robust API security measures, including multi-factor authentication and data encryption, to ensure the security of its API-powered services.

Navigating the Legal and Regulatory Landscape of Open Banking and APIs in Banking:

The legal and regulatory landscape of open banking and APIs in the banking industry can be complex and challenging to navigate, with different countries having different laws and regulations.

Banks in Africa must be aware of these laws and regulations, including data protection regulations such as the General Data Protection Regulation (GDPR), And the Protection of Personal Information Act (POPI) in South Africa, to ensure compliance and offer secure and reliable API services to their customers.

The Intersection of Artificial Intelligence and Open Banking in Banking:

The integration of artificial intelligence (AI) and open banking has the potential to revolutionize the banking industry by providing customers with personalized financial advice, improving the efficiency of banking processes, and reducing costs.

For example, Standard Bank has integrated AI into its open banking platform, enabling customers to access personalized financial advice and recommendations based on their unique financial situation.

The Impact of Open Banking on Consumer Banking Services had ensured more financial inclusion and autonomy.

For example, First National Bank has leveraged open banking and APIs to launch its “FNB Connect” platform, which allows customers to manage their finances, make payments, and access financial services from a single platform.

Banks in Africa that embrace these technologies will be well positioned to take advantage of new opportunities for growth and innovation.

For example, Ecobank, one of the largest pan-African banks, has used APIs to launch its “Ecobank Fintech” platform, which provides access to a range of financial services and

SOURCES:

]]>

Decision-makers in banking expressed concerns about moving their operations to the cloud. This is understandable. There were recent data breaches during cloud migrations at Capital One and T-Mobile

Yet, with planning, you can avoid these mistakes and reap the benefits of cloud migration.

The Cloud Security Alliance conducted a study. They found that organizations had three times the chance of success with a plan. Also, a study by the IBM Institute for Business Value found planning reduced costs by up to 30%.

In this blog, Banks will learn from the mistakes of others during cloud migration. Banks can also modernize their IT infrastructure and maximize cloud computing. All the while not compromising the security and compliance of sensitive financial data.

- Mastering the Art of Cloud Migration: How a Detailed Plan Can Benefit Banks

The Cloud Security Alliance conducted a study. They found that lack of proper planning is one of the top three causes of cloud migration failure. Organizations with detailed migration plans were three times more likely to be successful.

This plan should include timelines, milestones, and contingencies to help manage the process. It should also include a thorough assessment of the bank’s current IT infrastructure. That way, any potential roadblocks get addressed early.

A detailed plan also helps banks to reduce costs and improve efficiency. The IBM Institute for Business Value also did a study. They found that organizations with clear migration plans reduced their costs by up to 30%.

Cloud migration allows banks to modernize their IT infrastructure and maximize cloud computing. “But, failure to plan can lead to migration failure,” says the Cloud Security Alliance.

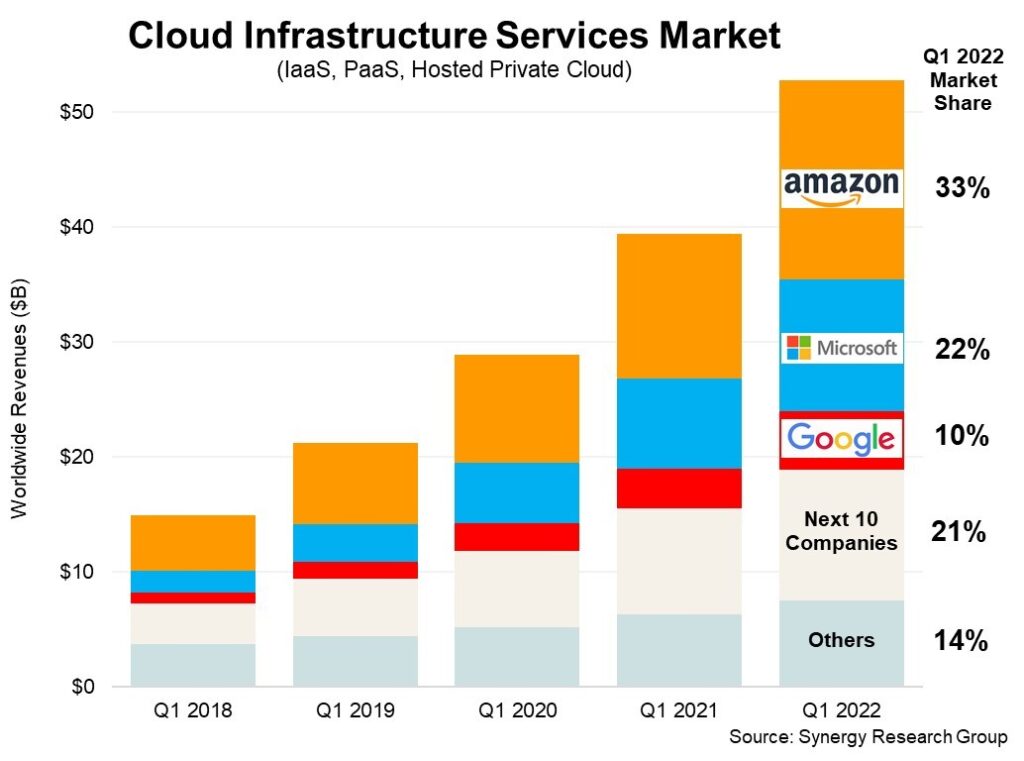

- Navigating the Cloud: How to Choose the Best Provider for Your Banking Needs

When choosing a cloud provider for your banking needs, consider the following factors:

- Data security and compliance with industry regulations

- Reliability and scalability.

- The provider’s global network,

- Provider experience working with financial institutions

- Pricing and contract terms.

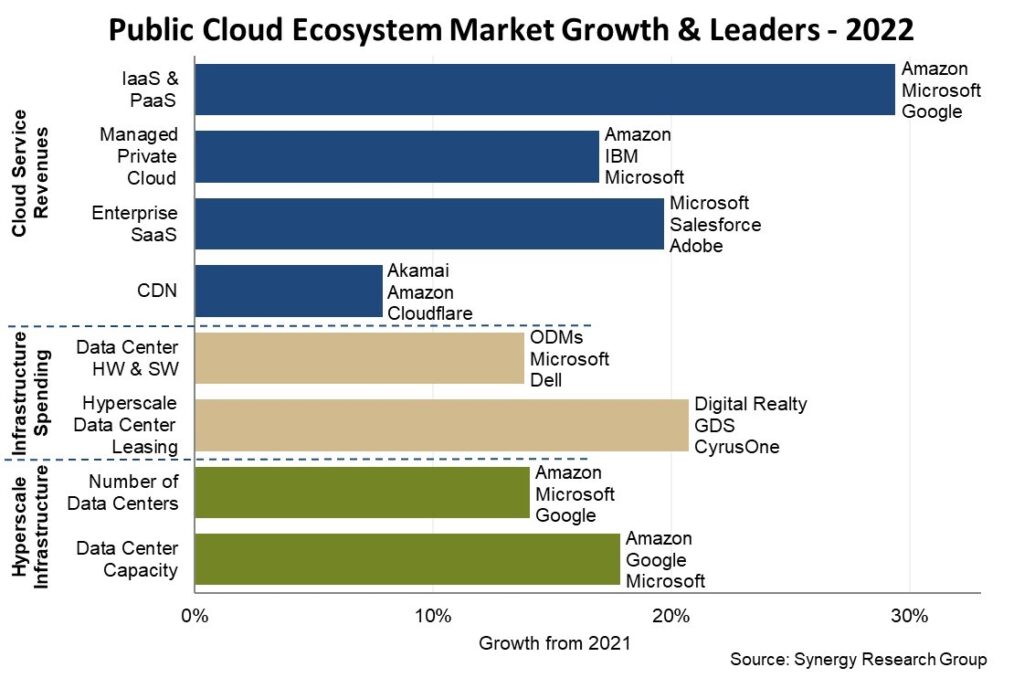

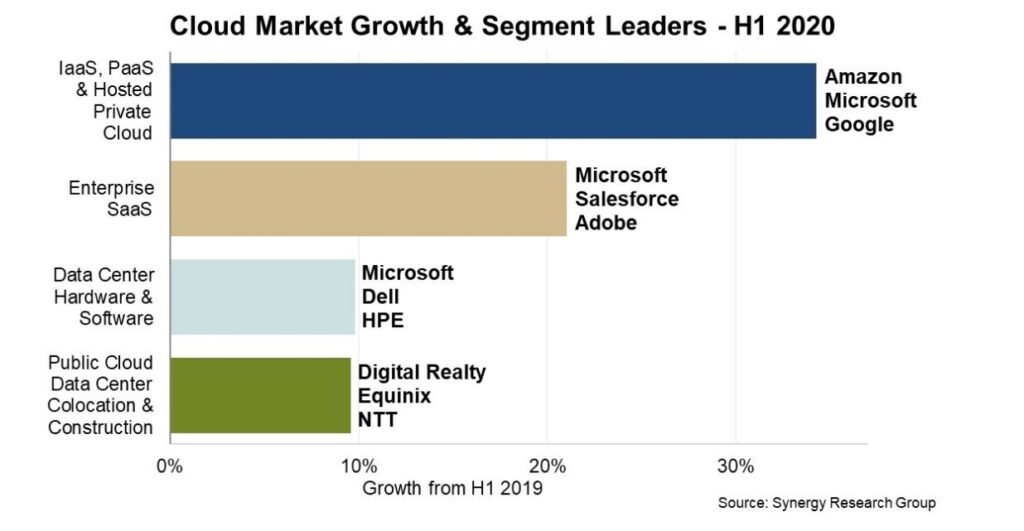

Some of the top cloud providers in the banking industry include:

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

According to a 2020 report by Synergy Research Group. AWS has the largest share of the market. Their infrastructure-as-a-service (IaaS) and platform-as-a-service (PaaS), had 33% of the market share. Microsoft Azure and Google Cloud followed with 18% and 8% market shares. You can read about this research at this link.

Also, note that large banks have their own private cloud infrastructure. They manage and operate it in-house.

In the end, the best cloud provider for your needs will depend on your specific requirements. So, analyze your options. Also, a trusted advisor or consultant can help you make an informed decision.

- Cloud Migration 101: The Importance of Testing and Training for a Seamless Transition

Testing allows you to identify and address any issues before the migration goes live. This can include functional testing, performance testing, and security testing. Performing these tests verifies that systems and applications are working as expected. They also identify and address potential problems.

Another important aspect of successful cloud migration is training. Your employees should get training on the new systems and applications. This includes new cloud platforms, and new or updated software and tools. Training speeds up new technology usage in day-to-day operations.

The International Data Corporation (IDC) conducted a study. It found that organizations that test and train staff and solutions; enjoy higher returns on investment (ROI). It also indicated an average of 30% faster migration and 25% higher ROI.

In summary, testing and training are essential components of successful cloud migration. Test your systems and applications and train your employees. You will ensure a smooth transition to the cloud and a higher return on investment.

- Cloud Migration for Banks: How to Ensure Compliance and Secure Your Data

When migrating to the cloud, banks in Africa must consider the following.

- Various regulations and compliance requirements specific to the region

- Security of sensitive financial data.

The first example is the Central Bank of Nigeria (CBN) guideline on electronic banking. It requires the security and integrity of electronic banking operations. This includes having a disaster recovery plan and incident management plan. Banks must ensure that their cloud provider is compliant with these guidelines. Also, have the necessary controls in place to protect against data breaches.

The second is the African Continental Free Trade Agreement (AfCFTA). It came into force in January 2021. The AfCFTA requires the free movement of goods, services, and people, across borders. Banks must ensure that their cloud provider is compliant with this agreement. Besides, having the necessary controls to protect the personal data of African citizens.

Additionally, African banks should also adopt these security practices:

- Encrypting sensitive data both at rest and in transition.

- Implementing multi-factor authentication for access to cloud systems

- Monitoring and auditing cloud systems for security vulnerabilities

- Having a robust incident response plan in place for security incidents.

Note that in Africa cloud technology adoption is still in its early stages. Thus, banks are learning to navigate the complexity of regulatory compliance and security. African banking security experts or IT consultants are the best advisors on this.

- Maximizing Cloud Migration Success: The Importance of Monitoring and Optimizing Your Infrastructure

Monitoring ensures systems are performing and you have the resources you need. This includes monitoring key metrics such as

- CPU usage,

- Memory usage

- Network traffic

- Storage usage

Additionally, monitoring cloud infrastructure costs reduce spending on under-utilized resources.

IDC conducted a study in 2020. organizations that track and optimize their cloud infrastructure enjoy many benefits, these include

- Increased system performance

- Reduced costs

- Improved security.

These organizations enjoy a 20% system performance increase and a 30% cost reduction. But, note that the level of cloud adoption in Africa is still low, and the cloud market is new.

Furthermore, Africa lacks the infrastructure and skilled IT professionals for the cloud environment. As a result, monitoring and optimizing cloud infrastructure is a challenge.

- Avoiding Pitfalls: Common Mistakes to Avoid in Cloud Migration for Banks

Here are a few of the most common mistakes to avoid when migrating to the cloud in Africa. All the following mistakes are in this blog.

1. Lack of a clear migration plan

2. Not considering regulatory compliance

3. Failing to test systems:

4. Lack of training for employees

5. Not monitoring and optimizing the cloud infrastructure

IDC conducted a study on these mistakes. They result in 50% longer migration times and 25% higher costs. Furthermore, these mistakes cause system downtimes, data loss, and security breaches.

- Data Migration in Cloud Migration for Banks: Why it’s Important and How to Do it Right

Moving data from on-premise systems to the cloud is complex and time-consuming. But is a must for the success of the migration. Data migration helps to improve data security, compliance, and all operations.

Accenture conducted a study on data migration. It is among the challenging aspects of cloud migration. For over 60% of banks, data migration is the most difficult step. This is because of the complexities of preparing, transferring, and validating data. Additionally, dealing with data quality issues and ensuring data consistency.

To ensure a successful data migration, test the migration to ensure it is seamless. This way data is not lost or compromised.

Another important aspect of data migration is data security. This includes implementing encryption, multi-factor authentication, and other measures for sensitive financial data.

Follow the above practices, for successful data migrations. It also prevents data loss or compromise.

- Steady and Sure: The Importance of a Well-Planned Cloud Migration for Banks

Cloud computing improves operations and customer experience.

One of the other benefits of migrating to the cloud is higher scalability. With cloud computing, banks can add or remove resources as needed. They don’t need to invest in new hardware.

In Africa, there is rapid population growth and economic development. Also, the digital native market had led to increased demand for financial services.

The second benefit of migrating to the cloud is security. Banks in Africa face many unique security challenges. These include a lack of physical security infrastructure and trained personnel. Moving to the cloud can take advantage of the latest security technologies. For example, multi-factor authentication and encryption, protect their customer’s sensitive information.

Yet, migrating to the cloud is not without its challenges. One of the biggest challenges is minimizing the disruption of banks’ operations. Also, infrastructure and personnel are in place to support the move.

To cut the risk of disruption, adopt a phased approach to their cloud migration. This involves moving workloads to the cloud in stages, rather than all at once. Through this approach, you test the waters and address issues before a commitment.

Declouding: Moving Away from the Cloud

Declouding refers to moving away from cloud computing and returning to on-premises infrastructure. It is becoming a popular trend among African businesses.

Although cloud computing has benefits there are reasons why businesses choose to decloud.

One of the main reasons for declouding in Africa is the cost. While cloud computing can be cost-effective in the short term, over time, the costs can add up.

The costs of cloud computing, such as data storage, bandwidth, and maintenance, are high. Additionally, as businesses grow, they need more resources, leading to increased costs.

Another reason for declouding in Africa is data sovereignty. In cloud computing, third-party providers store and manage businesses’ data. This can be a concern for regulated industries, as they have strict data protection laws. By declouding, these businesses regain control over their data. They also follow local regulations.

A third reason for declouding in Africa is security. While cloud computing can offer improved security, it also comes with its own set of risks. Businesses worry about the security of their data housed in a third-party data center. Especially in countries where cybercrime is prevalent. By declouding, businesses take a more proactive approach to security. They store and protect their data to meet their specific needs.

Finally, many businesses decloud because they want to take advantage of new technologies. As technology continues to evolve, businesses’ initial technology can’t support their needs. By declouding, businesses take advantage of new technologies. For instance, edge computing provides more efficient and cost-effective solutions than cloud computing.

This podcast discusses reasons why 37signals decided to move away from cloud services and host their software on their own servers.

- Cloud services have been around for over a decade and many companies are starting to question their use.

- Companies with a predictable base load and a long-time horizon may benefit from hosting their own software.

- Purchasing hardware is now more affordable than ever.

Counter arguments:

- Cloud services offer simplification benefits that may be worth the cost.

- Companies with unpredictable loads may not benefit from hosting their own software.

Work with us

Looking for a reliable partner for your cloud migration journey?

Finsense is here to help with comprehensive roadmaps, support, and expert guidance every step of the way. Contact us today and let our years of experience ensure a smooth transition for your business.

Sources

- Capital One data breach: https://www.cnn.com/2019/07/29/tech/capital-one-data-breach/index.html

- T-Mobile data breach: https://www.csoonline.com/article/3480286/t-mobile-data-breach-was-caused-by-a-misconfigured-firewall-during-an-aws-migration.htmlTop of Form

Introduction

When it comes to discussing Open Banking, Open APIs in Banking, BIAN APIs, and Banking as a Service, it’s important to understand that these are all different concepts that relate to the same singular idea of giving third parties access to a bank’s data and/or functionality so they can create new or different experiences and products for customers.

Although people often use these terms interchangeably, it’s important to understand the distinctions between them so you can better understand the role each one plays in the world of banking.

In this article, we will explore the differences and similarities between various concepts with David Roldan, an API expert from Sharper. We will also give an overview of what is happening in Africa.

Open Banking

Open Banking is a network of financial institutions that share data using APIs. By opening these APIs to sharing, 3rd parties have easier access to financial information, which allows them to build new and different apps and services.

Financial institutions have been hesitant to participate in open banking because it would mean competing with one another; however, regulators have been urging them to do so. This is true for the Open Banking Standard in the United Kingdom and the PSD2 in Europe. In other regions, though, open banking is being driven by market dynamics.

Developers can use Open Banking APIs to access a limited set of features such as account aggregation and payment initiation. We recommend looking at the regional standards to see what standards are available in your area.

Open APIs in banking

APIs allow information to be shared between different systems, whereas open APIs refer to a publicly available interface that allows data or functionality to be shared. Open APIs in open banking allow third parties to access a financial institution’s customer data (with the customer’s permission) or the financial institution’s service offerings and functionality. This is significant because it allows customers to have more control over their data and allows third parties to provide value-added services to customers.

BIAN APIs

The Banking Industry Architecture Network (BIAN) is a model of business capabilities, scenarios, service domains, and business objects used in banking and other financial services. This enables cost reduction and management change by developing digital standards and best practices in service-oriented architecture and banking APIs.

The BIAN APIs are a set of banking-related APIs that support the partitions and service operations of the BIAN Service Domain. They are built in a RESTful architecture style, making it simple for organizations to incorporate them into their API management strategy. This speeds up time-to-market and improves banking best practices for financial organizations that adopt them.

The BIAN APIs are a set of service operations that are designed to make it easier for global banks to adopt modern banking interoperability standards. These APIs are not required, but they can be used to simplify digital transformation. In addition, Open Banking APIs and Open APIs for Banking can be built on top of the BIAN APIs.

Banking as a Service (BaaS)

Banking as a Service (BaaS) may sound similar to open banking at first, but there is a crucial difference between the two. While open banking provides third-party access to the data of existing bank customers, BaaS provides access to bank functionality so that non-bank companies can connect users outside of the bank’s existing customer base to banking services. In other words, open banking gives third parties access to data that’s already there, while BaaS allows for the creation of new data sets and connections.

Banking as a Service provides a company with the ability to construct its own customer experience, under its brand name, with the support of a bank’s existing infrastructure and specialist knowledge. This allows providers to create a unique and differentiated offering for their customers.

Banking Transformation: An African Perspective

Like in other industries, banking in Africa has evolved to take advantage of new technologies. For example, with the advent of mobile phones, 96% of Kenyans now use MPESA, a fintech for mobile money transfers and payments. 10% of all people using mobile banking in the world are Kenyans.

PSD2 was supposed to come into effect five years ago, but due to negotiations, it only just came into effect in 2019. Many developed countries have “old” banking systems that make any modern progress look like a mistake. However, Africa’s banking infrastructure is not yet fully developed, so modern technology has not caused as much destruction on the continent. Some experts refer to Africa as a “greenfield” for open banking.

Challenge

Open Banking and BAAS both face challenges and opportunities in Africa, a key market for these technologies. Open banking has the potential to shape and improve financial systems around the world. Africa, in particular, faces obstacles and challenges that make it difficult to use traditional banking methods. For example, 50% of Africans do not have a bank account.

There are still very few working banking APIs in Africa. Many countries in Africa lack traditional banking infrastructure or banking licenses operated by technology companies. In addition, regulators have been slow to provide policies and frameworks for open banking. For example, the central Nigerian, Rwandan, and Kenyan banks recently launched open banking frameworks.

This scarcity of working APIs presents a challenge for FinTech companies operating in Africa, which must rely on other means for customer acquisition and data distribution. For African startups working on innovative solutions to improve financial inclusion, this lack of access to banking infrastructure can be a roadblock to success.

Outliers

Banking APIs have the potential to improve access to financial services for Africans living on the continent, but they are primarily only available in a few countries like Kenya, Nigeria, and South Africa. This is promising, but companies are still struggling to make these APIs work properly.

API fintech companies like Mono and Okra from Nigeria are leading the way when it comes to the potential future of API banking. With the continent’s economy growing, more and more tech-savvy Africans can spend money on apps and online services. This presents a huge opportunity for both banks and non-banks to enter this market and become interoperable financial service providers.

Solution

“Africa has great potential” is no longer a slogan, but rather a harsh reality for many fintech companies. Financial exclusion has been a major setback, as millions of people in Africa remain unbanked. This lack of access to customer data makes it difficult for fintech companies to compete with those in developed countries. Fintech companies should also keep security and customer data a priority to avoid the challenges faced by the first European PSD.

Second, APIs can help banks overcome infrastructure challenges. In general, the term “API” refers to an open API that can be integrated with third parties. However, they can also help build robust business architectures that are flexible and modular. This way, they can offer more value to customers who use them.

Fintech has the potential to revolutionize banking in Africa by making financial services more accessible and affordable. However, there is still work to be done before open banking APIs are up and running smoothly on the continent.

Conclusions

The advent of the API economy has largely changed the way banks and financial technology companies operate within the financial services industry. APIs (Application Programming Interfaces) provide a digital link between the IT systems of an enterprise and play a crucial role in a bank’s digitization process. By connecting a bank’s IT ecosystem with various internal and external systems and digital channels, APIs help banks exploit significant competitive advantages.

Africa is gradually catching up to other continents in terms of open banking development. Although we haven’t seen a comprehensive open banking framework emerge just yet, individual countries are taking strides toward digital transformation. A few African nations have even become leaders in open banking regulatory frameworks.

Sources:

What Is Open Banking? – Forbes Advisor

Open Banking & Banking APIs Explained W/ Examples (insiderintelligence.com)

Banks are open to open banking: Better ways to work with FinTech (bai.org)

]]> database can optimize your business’s virtualised computing

database can optimize your business’s virtualised computing  environment. Improved agility and innovation can help your business unlock greater value.

environment. Improved agility and innovation can help your business unlock greater value.

Source : @forbes

]]>Containers use something called ‘Virtualization’. But, what is Virtualization?

Well, virtualization is a concept that lets a single machine be divided into multiple machines virtually. These virtual machines run in isolation from each other.

It enables a container to work with just the source code along with basic dependencies and leverage the host machine’s resources to be small, fast, and portable.

Containers also enable the micro-services approach which provides advantages to businesses.

They enable easy management of code, better scalability, quicker time to market, and are more fault-tolerant.

Moving from VMs to containers also lets you take advantage of Cloud Native architecture which is fast becoming the norm for all the leading businesses.

We at FinSense can help you with containers and move towards cloud-native architecture!

]]>