The future of finance is changing rapidly. Over the past decade, advanced machine learning has taken over many tasks that humans previously performed.

From self-driving cars to smart phones, these technologies have advanced at an exponential rate. Now, new technologies are emerging that use artificial intelligence (AI) to complement existing processes and provide insights that allow people to make better decisions.

In November 30th 2022 Open AI launched ChatGPT. By December 4th the open platform had over a million users, breaking the records other popular platforms.

Facebook took up to 10 months before accumulation one million users. Twitter took up to 2 years to get to a million users. Last but not least, TikTok, The Open AI innovation received up to 1million users in 24 hours.

The amount of posts on LinkedIn and YouTube about the supposed solution to all repetitive tasks were uncontrollable. Experts have mixed reactions to the possibilities of AI, some agree that it’s impact has been far-reaching and positive so far.

Understanding the impact of AI on finance services

Today, AI is an integral part of our lives. From self-driving cars and video games to Netflix’s recommendation engine and Facebook’s algorithm, AI is no longer just in our pocket (it’s in everything).

But what has this changed for the financial services industry? What are the biggest risks and opportunities that it can bring? And how will AI impact your role in finance moving forward?

According to the mckinsey-tech-trends-outlook-2022-research-overview.pdf Applied AI received $165 billion investment funding in 2022.

Through the machine learning Canonical stack, we are witnessing the democratization of AI. The use of artificial intelligence will aid in the management of credit card fraud risks and the prevention of losses.

The benefits of AI in the financial industry

The benefits of AI in the financial industry are manifold. The technology is expected to reduce the costs of customer service and improve efficiencies across all stages of the process. It will also enable banks to enhance their product offerings and offer tailor-made services to customers.

The introduction of AI technologies is expected to provide financial institutions with a competitive advantage, enabling them to better adapt to the rapidly changing market environment.

AI has been a major buzzword for years now and has become a popular topic of discussion as we aim to reinvent our future. As AI becomes mainstream here are some benefits the financial industry will enjoy:

● Lower costs by automating repetitive tasks that take up a lot of time.

● Improved customer experience through personalized recommendations and personalization.

● Improved efficiency by utilizing machine learning algorithms to make better decisions.

● Increase in revenue through improved market research and analysis.

The financial services industry is undergoing a transition as AI becomes more pervasive. It’s no longer about the mythical replacing humans with machines, but leveraging artificial intelligence to better serve customers and improve operations.

In fact, AI can play a key role in helping banks and other financial institutions create value for their customers and deliver a better customer experience.

Here are some ways AI will improve the customer’s journey:

1. Improving customer service: Analyzing data from transactions and account activity to identify trends that can be used for predictive analytics. For example, AI could analyze historical transaction data and identify trends such as when customers purchase certain products or make payments on time. This allows banks to predict which customers might need assistance in the future.

2. Automating tasks: AI can automate many of the tasks currently done manually, freeing up employees for customer support. For example, an AI system might be able to integrate information from multiple sources, such as account statements, credit scores and social media posts, into a single report that shows the entire picture of your finances in real time.

3. Predicting client behavior: With enough data about customers’ past spending habits, an AI system could predict what they’re likely to want in the future.

4. Decision support systems, which are based on data analysis and machine learning algorithms, can assist in making financial decisions (DSS).

The impact of AI on finance is that it can automate many manual tasks, freeing up time and resources for humans to focus on higher-value activities. These include:

1. Predicting future events, such as the weather or stock prices, which could be used to make better investment decisions.

2. Creating original content, such as articles and videos, which can be shared with customers in order to drive engagement and loyalty.

3. Insights into customers’ behavior and preferences, which will help them understand how best to serve them. AI can analyze large amounts of financial data to forecast future outcomes or trends, a process known as advanced analytics or big data analytics (aka BDaaS).

Predictions for the adoption of AI in 2023

Artificial intelligence (AI) leaders, consultants and vendors looked at enterprise trends and made their predictions. After a whirlwind 2022, here are some quoted highlights of their insights:

1. AI will be at the core of connected ecosystems —–Vinod Bidarkoppa, CTO of Sam’s Club and SVP of Walmart

In 2023, we’re going to see more organizations start to move away from deploying siloed AI and ML applications that replicate human actions for highly specific purposes and begin building more connected ecosystems with AI at their core.

This will enable organizations to take data from throughout the enterprise to strengthen machine learning models across applications. Hence effectively creating learning systems that continually improve outcomes.

For enterprises to be successful, they need to think about AI as a business multiplier, rather than simply an optimizer.

2. AI will create meaningful coaching experiences— Zayd Enam, CEO, Cresta

Modern AI technology is already being used to help managers, coaches and executives with real-time feedback to better interpret inflection, emotion and more, and provide recommendations on how to improve future interactions.

The ability to interpret meaningful resonance as it happens is a level of coaching no human being can provide.

3. AI will empower more efficient DevOps – Kevin Thompson, CEO, Tricentis

When it comes to devops, experts are confident that AI is not going to replace jobs; rather, it will empower developers and testers to work more efficiently. AI integration is augmenting people and empowering exploratory testers to find more bugs and issues upfront, streamlining the process from development to deployment.

In 2023, we’ll see already-lean teams working more efficiently and with less risk as AI continues to be implemented throughout the development cycle.

“Specifically, AI-augmentation will help inform decision-making processes for devops teams by finding patterns and pointing out outliers, allowing applications to continuously ‘self-heal’ and freeing up time for teams to focus their brain power on the tasks that developers actually want to do and that are more strategically important to the organization.”

4. AI investments will move to fully-productized applications — Amr Awadallah, CEO, Vectara

There will be less investment within Fortune 500 organizations allocated to internal ML and data science teams to build solutions from the ground up. It will be replaced with investments in fully productized applications or platform interfaces to deliver the desired data analytic and customer experience outcomes in focus.

That’s because in the next five years, nearly every application will be powered by LLM-based neural network-powered data pipelines to help classify, enrich, interpret and serve.

But productization of neural network technology is one of the hardest tasks in the computer science field right now. It is an incredibly fast-moving space that without dedicated focus and exposure to many different types of data and use cases, it will be hard for internal-solution ML teams to excel at leveraging these technologies.

References

ai-trends-for-2023-industry-experts-and-chatgpt-ai-make-their-predictions/

AI is Changing Financial Services Delivery

AI is transforming the way businesses operate and invest, enabling them to identify patterns, make predictions, create rules, automate processes, and communicate more efficiently.

It is at the top of the agenda for financial services, as customers are becoming more informed and expect transparent as well as consistent and reliable services.

To generate value, banks and financial services organizations should be smart about choosing appropriate use cases and technologies. These use cases should outline what “measurable” success looks like both in the short and long term and should be assessed and prioritized based on the level of business impact and technological feasibility.

For example, classification type problems are commonly seen in banking, and AI-driven call center compliance automation is an example of using AI to classify high-risk calls for further review.

Mariette van Niekerk leads the Data Science & AI practice of Deloitte New Zealand’s Risk Advisory team, using a variety of machine learning / AI technologies to detect and manage fraud and operational risks.

She is a seasoned data scientist and project manager with a 12-year track record of delivering cross-industry operations research and artificial intelligence solutions. She recommends breaking the high-level plan for full roll-out down into smaller phases that deliver benefits early.

References

“How AI Is Shaping the Future of Financial Services.” Deloitte New Zealand, 18 May 2022

Challenges of Adopting AI in the Financial Industry

The use of AI in global banking is estimated to grow from a $41.1 billion business in 2018 to $300 billion by 2030. Traditional financial services companies have two objectives to fulfill with AI: speed, flexibility, and agility, and adhering to compliance standards and regulatory requirements.

However, big challenges remain in building responsible and ethical AI systems, and traditional financial institutions struggle to deploy in-depth AI capabilities to truly harness its full potential.

These include:

Data quality and weak core structures make it difficult for AI and ML systems to identify overlapping and conflicting entries.

Lack of support for AI-specific scale and volume and can even show biased results when written by developers with a biased mind.

Lack of standard processes and guidelines for AI in the financial domain.

The lack of talent, budget constraints.

Significant commitment toward AI investment. It is important to consider the context, use case, and type of AI model implemented to analyse the appropriate approach while collaborating or upscaling core tech systems.

The Economist’s research team found that 86% of Financial Service executives plan to increase AI-related investment over the next five years, with the strongest intent expressed by firms in the APAC and North American regions.

Businesses that scale with AI over time, will enjoy an unwavering focus on compliance, customer satisfaction, and retention.

References

AI Adoption Challenges in Traditional Financial Services Companies, 7 Mar. 2022

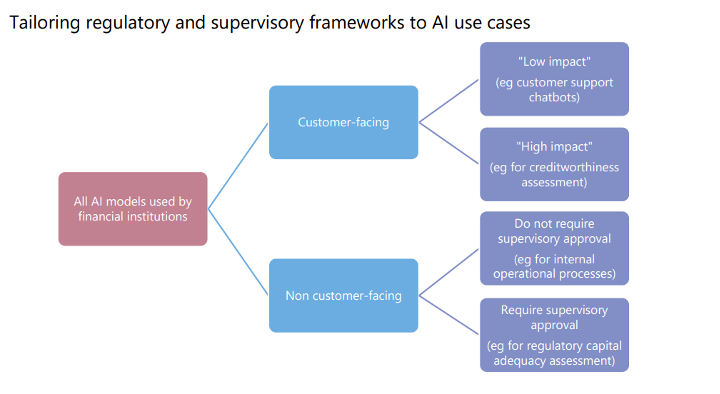

Role of Government and Regulatory Bodies in Financial Services AI

AI, including machine learning (ML), can improve the delivery of financial services as well as operational and risk management processes. Financial authorities are encouraging financial sector innovation and the use of new technologies.

As a result, sound regulatory frameworks are required to maximize benefits and minimize risks from these new technologies. There are AI governance frameworks or principles that apply across industries, and several financial authorities have begun developing similar frameworks for the financial sector.

These frameworks are based on general guiding principles such as dependability, accountability, transparency, fairness, and ethics. Financial regulators are under increasing pressure to provide more concrete, practical guidance.

Existing governance, risk management, and development and operation requirements for traditional models also apply.

Businesses can benefit from this financial industry behemoth of JP Morgan. This section examines how one of the largest banks, JP Morgan Chase & Co. is using artificial intelligence to tackle a slew of mundane tasks.

The multinational is unwavering in its commitment to lowering costs, increasing operational efficiency, and

improving the client experience, and it has been an early adopter of disruptive technologies such as Blockchain.

They established a center of excellence within Intelligent Solutions in 2016 to investigate and implement a

growing number of use cases for machine learning applications across the organization.

They have a document review system, in which corporate lawyers analyse large amounts of data and sort and identify important pieces for litigation, which is one of the legal profession’s pain points.

According to a McKinsey & Co. study, nearly a quarter of lawyer work output can be automated. According to a study conducted by Frank Levy at MIT and Dana Remus at the University of North Carolina School of Law,

implementing machine learning could reduce lawyers’ billable hours by about 13%.

JP Morgan has also implemented a program called COiN, which uses unsupervised machine learning to automate the contract document review process. The primary technique employed is image recognition, and the algorithm can extract 150 relevant attributes from annual commercial credit agreements in seconds, as opposed to 360,000 person-hours for manual review.

COiN is proving to be more cost-effective, efficient, and error free, and the company is committed to its technology hubs for teams specializing in big data, robotics, and cloud infrastructure in order to find new revenue streams while reducing expenses and risks.

References:

“AI in Banking: A JP Morgan Case Study and Takeaway for Businesses.”

Conclusion

In conclusion, the current state of Artificial Intelligence in banking is rapidly evolving and has the potential to greatly improve the efficiency and accuracy of financial services. AI-powered solutions can help banks with tasks ranging from fraud detection to customer service and personalization.

However, the implementation of AI in the banking sector must be done with caution and proper regulations in place to ensure the safety and privacy of customers’ data and to prevent any potential biases in decision making.

As AI continues to mature, it is expected to bring significant benefits to the banking industry and its customers, and it is essential for banking executives to stay informed and proactive in incorporating AI technology into

{kind=link}

0 Comments